How to translate insurance to your compliance team

Does your compliance staff fully understand the ins and outs of certificates of insurance (COIs), endorsements, and insurance coverage? Even those who work with the documents and processes every day have difficulty keeping up with the ever-changing regulations of the complex insurance industry, which could leave your organization exposed to risk.

A costly lawsuit or insufficient coverage limits that force your organization to payout a claim are just two ways that risk exposure can harm your business. No matter how well you train your compliance staff, here’s why compliance can still present challenges to them, and how you can address those challenges.

Insurance Add-ons / Endorsements Can be Complex

When a judge rules on a case that changes the interpretation of insurance clauses, it has a ripple effect across the insurance world. But this impact could take a while to reach your insurer and then to your compliance staff.

Insurers respond to case law changes and precedents by adjusting endorsements and requirements. There are over 1,000 endorsements available for numerous specific scenarios, adding to the complexity of the documents your staff reviews. Additional insured endorsements can provide coverage for:

- The sole negligence of the additional insured;

- The additional insured only for the named insured’s negligent acts; or

- Particular projects or a particular activity.

In each area, the endorsement’s language and the jurisdiction’s interpretation of that language limits the scope of the coverage provided. Unless compliance staff is constantly reading and staying up to date on the law, it’s easy for them to overlook an important piece of information. Since they likely have other responsibilities, anything you can do to make the COI review process more efficient reduces the worry that they’ll miss something that could harm your organization.

Laws for Every State are Different

State insurance laws vary - particularly when it comes to worker’s compensation. Each state’s schedule of benefits awards different amounts of monetary compensation for injuries to various parts of the body, for example.

When reviewing a limit, a compliance staff member could look at the names on a COI and see that your organization appears as an additional insured. They could think their job is done - but it’s not. There’s more to risk compliance than verifying limits and names on a COI.

Risk compliance should also look at exclusions, endorsements, and other items to see if they are sufficient to meet your state’s requirements. If your compliance staff isn’t careful to review beyond checking a few boxes, it puts your organization at incredible risk. If an injured employee filed a worker’s compensation claim, your insurance coverage might not be sufficient to cover the payout.

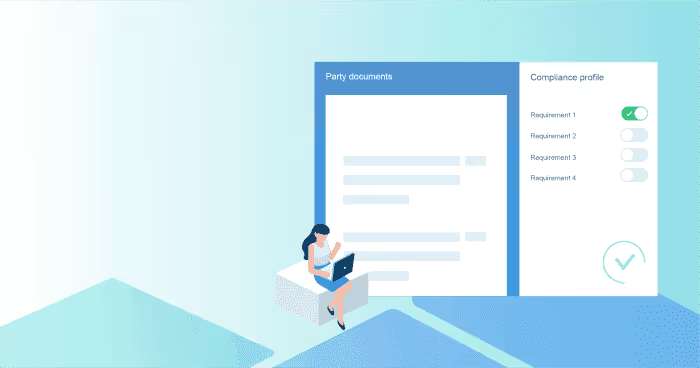

COI-tracking software like TrustLayer automatically checks that limits meet the minimums you set, which you can choose based on the laws in each state where you operate.

Outdated Tracking Methods Add Difficulties

How does your organization track COIs and compliance? If you started out with an Excel spreadsheet, your staff might still be adding rows and tick marks in columns. But, spreadsheets can easily and quickly become outdated.

If you have multiple staff members working in the same spreadsheet, version control and human error can also become issues. Who added that checkmark next to a major vendor’s COI? Did someone put the wrong expiration date in a column? There are more possibilities for error when you use a spreadsheet to track compliance.

Working in a spreadsheet also limits your ability to cross-check and verify data. To ensure accuracy, you’ll likely have to devote copious time to manual audits and following up on missed inputs. It’s time-consuming and costly to devote the necessary resources to verify the completeness and accuracy of a COI-tracking spreadsheet manually.

Automating the process in a platform like TrustLayer significantly reduces the possibility of error. The platform checks COIs and flags issues and missing data. It will even send follow-up emails to vendors to resolve errors and discrepancies.

Depending on the volume of COIs that your staff reviews annually, they might only have the time to scan a COI for the minimum when they’re relying on their own eyes as the verification system. Freeing up their time and lifting their administrative burden by partnering with a COI-tracking software that speaks insurance allows them to focus on addressing complex endorsements and other risk areas.