By Alicia Sandlin

The inability to subrogate a claim, or easily subrogate a claim, costs insurance companies time and money, and can even increase future risk. Explore the current process to better understand the best way to keep all the data you need easily accessible and ready for any new claim that arises.

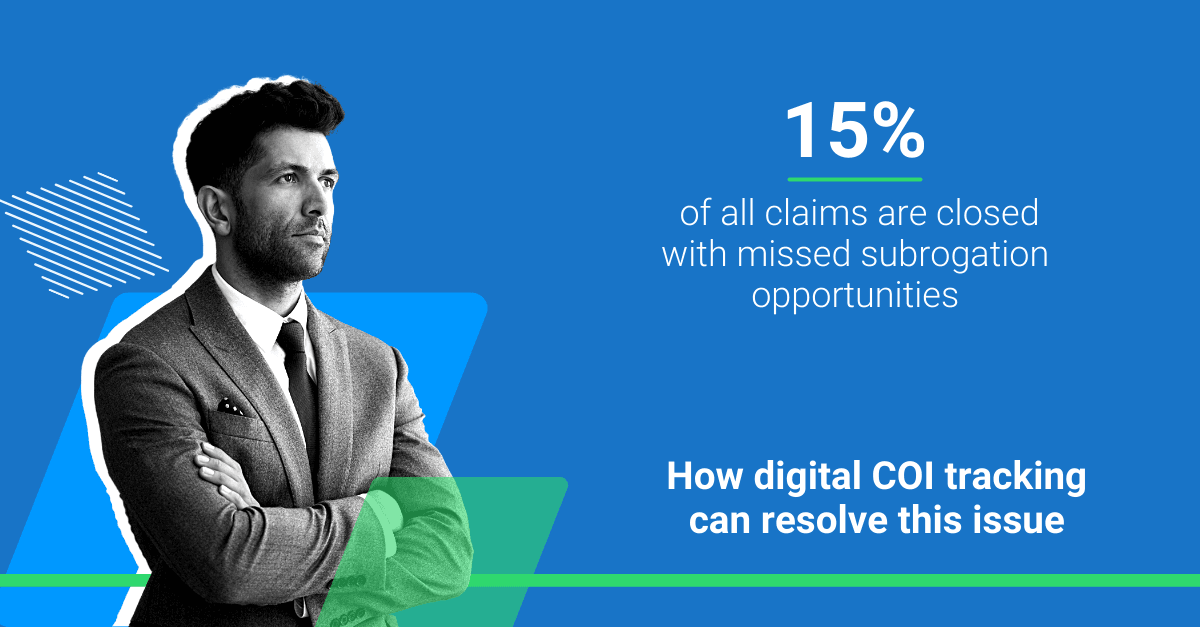

Believe it or not, roughly 15% of all claims are closed with missed subrogation opportunities, leaving the insurance industry with an outstanding bill of over $15 billion each year.

Insurers simply can’t afford to continue this way. A simple case of missing information often forces an insurer to pay for losses that aren’t really their responsibility. And inefficiencies within the subrogation process may leave insurers unsure of how to proceed.

Why COIs matter

Whether it’s a car totaled when hit by another driver or a contractor’s accident that caused damage on a site, subrogation recovery opportunities occur regularly. The key to efficiently resolving an issue is a readily available third party’s Certificate of Insurance (COI).

Insurers who actively track their vendors’ COIs are ahead of the game, since they can immediately move forward in the subrogation process. Those who aren’t tracking COIs may find it challenging to collect once there’s a claim.

The absence of a COI could mean many things: Maybe the third party doesn’t have insurance at all, or it’s expired. Maybe they never sent the information to you in the first place. And even if you do have all your data, locating a sheet of paper in a filing cabinet or a line of data in a spreadsheet can be a challenge.

In any of these scenarios, however, a missing COI costs insurers in a variety of ways, including:

- Money. Without the proper information (i.e., the COI), the insurer might have to pay the claim out of pocket.

- Time. Adjusters have to spend their time tracking down COIs, rather than focusing on resolving other claims.

- Risk. If the claim is open for a long time while you track down information, it can be hard to plan accordingly (i.e., reserve funds or properly underwrite future risk).

Ultimately, insurers depend on third parties to have reliable coverage as part of their risk management efforts, so they need the data to be readily available.

The claims journey

Whether the insurer has been actively tracking COIs or not, the existence of a valid COI becomes extremely important once there’s a claim.

Consider this real claims scenario: A claim is filed by a policyholder and enters the claims system. The claim is assigned to a claims adjuster, who is responsible for determining coverage according to the policy

- If the claim is covered, it can be processed. The claims adjuster will determine if it is the policyholder’s responsibility or if there is an opportunity for subrogation.

- If it is the third party’s responsibility, their COI becomes critical. Ideally, the COIs are actively managed and the paperwork is archived and easily accessible. The claims adjuster can simply provide the COI for the third party and proceed as normal.

- If the COIs are not tracked and available, the adjuster will need to go after their third party to obtain their COI. They need the proof, complete with the insurer, policy number and limits of the policy. With no real impetus to provide coverage, this often takes 6-12 months to resolve, on average.

The real issue here is the uncertainty. An insurer who has all relevant COIs knows there are recovery opportunities, even if it takes a while for them to materialize. This allows the insurance company to better understand the profitability of its portfolio and focus their efforts elsewhere.

A better way

Underwriters want to confirm their insureds are managing their risk by collecting third-party COIs. But if you are working with a number of vendors, it can be tricky to manage all the information manually. Because of this, underwriters prefer those who utilize a digital solution.

Imagine all the time you’d save, human error you’d eliminate, fraud you’d reduce, and risk visibility you’d gain if there was a way to trust in a digitized COI verification process with each one of your insured partners.

With TrustLayer, we can finally say there is.

About the author

Alicia Sandlin is a Director of Strategic Initiatives at TrustLayer, where she is responsible for driving demand and adoption for the industry-first Digital Proof of Insurance solution amongst insurance carrier partners. Alicia has nearly 20 years of multiline global insurance experience in managing a large-scale portfolio of enterprise clients, Underwriting, Global Casualty Auditing, and Portfolio Program Management. She is passionate about building meaningful connections with customers & partners and is a champion of diversity, equity, and inclusion.

Related Searches

coi for construction, coi for events, contractural risk transfer